Warren Buffett’s Moat Framework: Finding Economic Castles in the Market

Not All Competitive Advantages Are Created Equal

Here’s something that should bother you: fewer than 50 companies in the S&P 500 have actual economic moats. The rest? They’re pretending.

You’re probably invested in some of those pretenders right now. Treating their temporary wins like they’ll last forever. Watch the tech sector for five minutes and you’ll see how fast a “dominant” company can fall apart. What looked unbeatable today becomes irrelevant tomorrow.

This is why Buffett’s moat framework matters. The difference between getting rich and watching your portfolio bleed out usually comes down to one thing: does the company have a real moat?

What Actually Counts as a Moat

Think about a medieval castle. Strong walls help. But what really stops attackers is the moat. That water barrier makes breaching the walls too expensive to bother trying.

Your company is the castle. The moat is whatever stops competitors from doing what you do better, faster, or cheaper.

The problem? Most investors can’t tell the difference between a moat and a puddle. A puddle disappears the second the weather changes.

A company might dominate today because it has a hot product or a charismatic CEO. Looks like protection. Feels safe. It’s not. In 2025, with technology moving this fast and competitors everywhere, separating moats from puddles has become critical. Buffett figured this out decades ago. That’s why Berkshire Hathaway has crushed the market.

How Buffett Found This Edge

Buffett didn’t always hunt for moats. Early on, he followed Benjamin Graham’s playbook: find deeply discounted stocks trading at half their value. Buy them. You couldn’t lose much.

Then he evolved.

The breakthrough came in 1972 when Berkshire bought See’s Candies for $25 million. The company made about $2 million a year. By Graham’s math, you were paying twelve and a half times earnings for a candy company. His old investing buddies thought Buffett had lost it.

But Buffett saw something different.

See’s had built a brand moat over decades. California consumers loved it. They paid premium prices for chocolate that cost pennies to make. The company had pricing power, incredible margins, and steady demand that didn’t need constant reinvestment. A money machine.

The real insight? That moat would probably last thirty or forty years. Customers would keep buying See’s the way their parents had. That one deal changed everything about how he invested. Instead of hunting for cheap stocks, he’d hunt for great companies worth paying up for.

A wonderful company at a fair price beats a fair company at a cheap price.

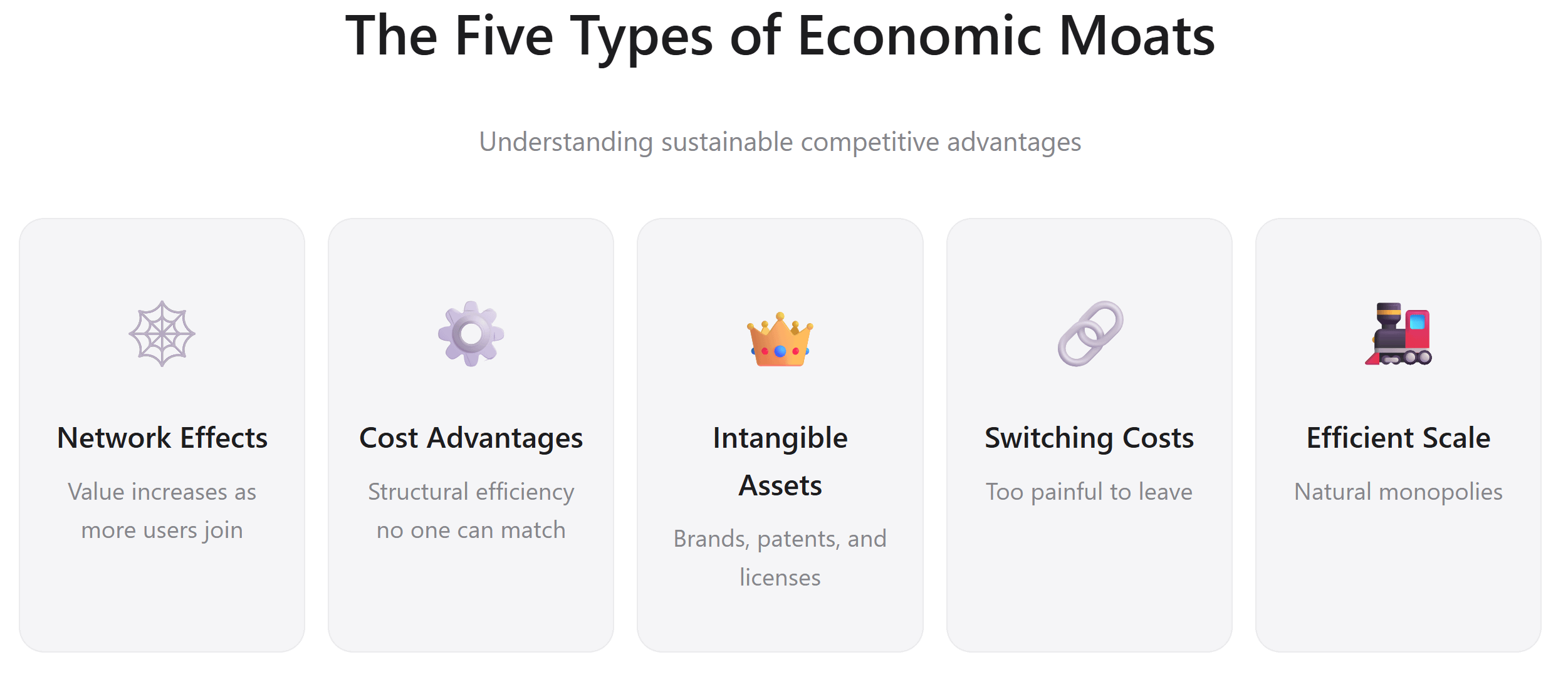

The Five Moat Types

Buffett and Morningstar identified five moat types. The critical thing to understand: the best companies stack multiple moats on top of each other. That’s when things get interesting.

The five types are network effects (the strongest), cost advantages, intangible assets (brands, patents, licenses), switching costs, and efficient scale.

Each works differently. Each is vulnerable to different threats. Each lasts for different lengths of time.

Network Effects: The Unbreakable Loop

Network effects might be the most powerful moat that exists. The product gets more valuable as more people use it. Not just that you want to use it because everyone else does. The thing literally becomes more useful.

Visa and Mastercard are the textbook example. Every merchant that signs up makes the network more valuable to cardholders. Every cardholder makes the network more valuable to merchants. A self-reinforcing loop that’s almost impossible to break.

Why is this moat so durable? Because disrupting a payment network means convincing millions of merchants and millions of people to switch at the same time. That’s an impossibly high bar. Even if someone built better technology, they’d still face the chicken-and-egg problem: merchants won’t accept your cards until customers want to use them, and customers won’t want to use them until merchants accept them.

Modern platforms work the same way. Airbnb gets better as more hosts join (more choices for travelers) and more travelers join (more demand for hosts). Once you hit critical mass, displacing you becomes nearly impossible because everyone’s already on your platform.

The real insight? Network effects create a first-mover advantage. Being first doesn’t guarantee success, but if you hit scale while operating a network effects business, you’ve built something extraordinarily hard to displace.

Cost Advantages: The Efficiency Game

Some companies build moats through pure operational efficiency. They make the same product cheaper than anyone else. This structural advantage is nearly impossible to copy.

Costco is the masterclass. The company operates on margins of five to ten percent. Sounds like suicide, except Costco has a secret weapon: membership fees. People pay upfront for the right to shop there.

This works in two ways. First, members feel they need to shop frequently to justify that membership fee. Second, that membership revenue covers almost all of Costco’s operating costs. The company can sell products at near-zero margins and still print money.

This creates a wall competitors can’t breach. Walmart tried to replicate the warehouse model but couldn’t compete. They lacked Costco’s scale and that membership revenue stream. You can’t suddenly start charging membership fees and expect to beat a company that already has established loyalty.

Walmart built a different cost advantage through its distribution infrastructure. When you run one of the world’s largest distribution networks supplying thousands of stores, you get enormous scale advantages. Suppliers have to work with you because you’re moving massive volumes.

Can Amazon’s scale overcome these traditional retailer moats? The answer’s complicated. Amazon has scale, but it operates at much higher costs and lower margins than Costco or Walmart. Amazon’s real moat isn’t in retail margins anyway. It’s elsewhere.

Intangible Assets: What Lives in People’s Heads

Some of the most durable moats don’t exist anywhere you can touch them. They live only in people’s minds. Yet they’re incredibly powerful.

Coca-Cola sells sugar water. You can buy identical ingredients from any grocery store for a fraction of what Coke charges. Yet Coca-Cola makes enormous profits because of what’s in people’s heads. Consumers choose it because they trust it, love it, and have emotional attachments built over a lifetime. That brand means the company can charge premium prices and command shelf space everywhere.

Disney stacks multiple intangible asset moats together. Its characters (Mickey, Elsa, Spider-Man) create licensing opportunities and drive people to theme parks. Its brand is trusted with families everywhere. Its content library means people want to watch Disney stuff, which makes them subscribe to Disney Plus.

Patents are another intangible asset moat, but with a catch: they’re temporary. A pharmaceutical company might have a patent on a blockbuster drug that creates a fifteen-year moat. When the patent expires, generics flood the market and margins collapse. Patents create moats only as long as the law protects them. That’s completely different from brand moats, which can last forever.

Switching Costs: The Pain of Leaving

Some companies build moats by making it painful to switch to someone else. These are some of the most profitable businesses you can own.

Microsoft is the obvious example. Once your office runs on Microsoft Office and your team knows all the shortcuts and workarounds, switching to Google Workspace becomes incredibly painful. Yeah, the functionality might be ninety percent the same. But the disruption of retraining everyone, migrating files, rebuilding templates, and rediscovering workflows is huge.

So you stay.

Adobe operates exactly the same playbook. Professional designers and photographers build entire workflows around Photoshop, Illustrator, and Premiere Pro. They’ve invested huge amounts of time mastering these tools. Competitors with potentially better technology can’t win because leaving costs too much.

Enterprise software companies milk this even harder. When a massive corporation runs its entire supply chain on SAP or its customer relationships on Salesforce, replacing that system is a multi-million-dollar, multi-year project. You don’t replace it on a whim. You only replace it if something’s fundamentally broken.

This gives these companies enormous pricing power and incredibly sticky customers.

Here’s the key: switching costs create loyalty that has nothing to do with loving the company. You’re loyal because leaving is expensive, not because the company earned your love.

Efficient Scale: The Natural Monopoly

Some industries can only support one profitable competitor because the capital requirements are absurdly high. These are the natural monopolies, and they create permanent moats.

Railroads are the classic. BNSF, owned by Berkshire Hathaway, and Union Pacific are the two largest railways in North America. But real competing railways don’t exist on their major routes. Why?

Building a second railroad network parallel to an existing one would cost hundreds of billions of dollars and be economically insane. You’d be splitting demand with a company that’s already recouped its infrastructure costs. You’d lose money for decades.

Local utilities work the same way. Once the infrastructure is built, the marginal cost of providing electricity, water, or gas to one more house is nearly zero. But building duplicate infrastructure would be ridiculous. So you end up with one utility per area. Natural monopoly. Built-in moat.

The trade-off: these moats come with regulation. The government allows the monopoly, but in return, the utility is regulated. Rates are controlled, profit margins are limited, service standards are mandated. You’re buying stability and durability but not explosive growth.

Moat Stacking: When Things Get Serious

This is what separates good investors from great ones. The best companies don’t rely on a single moat. They stack multiple moats on top of each other, creating exponential protection.

Apple ( AAPL 0.00%↑ ) is the modern masterclass. The company has a brand moat (people pay premium prices because of brand love and status). It has switching costs (your whole digital life is built around iOS, so switching to Android is a pain). And it has network effects (the more people on iOS, the more valuable the App Store becomes).

These three moats working together create a fortress. A competitor could make better hardware at a lower price. But the ecosystem lock-in makes leaving painful.

Amazon ( AMZN 0.00%↑ ) shows a different moat stack. It has cost advantages through massive scale in cloud computing and logistics. It has switching costs (AWS customers are deeply built into the platform). And it has network effects (the marketplace gets better as more sellers and buyers join). Prime membership is its own switching cost mechanism.

When multiple moats work together, they don’t just add. They multiply. A competitor trying to displace you has to overcome not one barrier but several at once.

Measuring What Actually Matters

Understanding moat types is one thing. Measuring how strong the moat actually is? That’s different.

Moat width measures your current competitive advantage. Return on invested capital (ROIC) tells you whether the company earns more than its cost of capital. If a company makes twenty percent returns on capital while competitors make eight percent, that’s a wide moat. Look at ROIC over more than ten years. A company maintaining superior returns decade after decade has a sustainable advantage.

Gross margin stability is another signal. Companies with real moats keep their margins high even as competition gets tougher.

Moat durability is about how long that advantage lasts. This is harder to measure but just as important. Ask yourself: what could destroy this moat in the next ten years? How fast is the technology changing in this industry? Could a well-funded startup displace this company?

For software companies, customer retention rates matter. For retailers, market share trends matter. For pharmaceutical companies, patent expiration dates matter. The specific metrics change by industry, but the principle stays the same: look forward ten years and ask whether this moat will still matter.

Red Flags You Can’t Ignore

Good investors constantly watch for signs that a moat is weakening.

Declining pricing power is the most obvious sign. If a company that commanded premium prices suddenly needs to discount to keep sales, the moat is shrinking.

Market share losses, especially to new entrants, suggest the moat isn’t working anymore.

Increased customer acquisition costs often mean the moat is weakening. If the company must spend more to acquire customers than it used to, it’s trying harder to overcome switching costs and network effects that used to work automatically.

Faster customer churn shows that switching costs are declining. If customers who used to stay forever are now leaving more regularly, something structural has changed.

Compressed margins are the ultimate erosion sign. When the company can’t maintain profitability while competitors gain share, the competitive advantage is slipping.

Key talent leaving for competitors often comes before bigger problems. When the best people exit, it’s usually because they see trouble.

The Puddle Problem

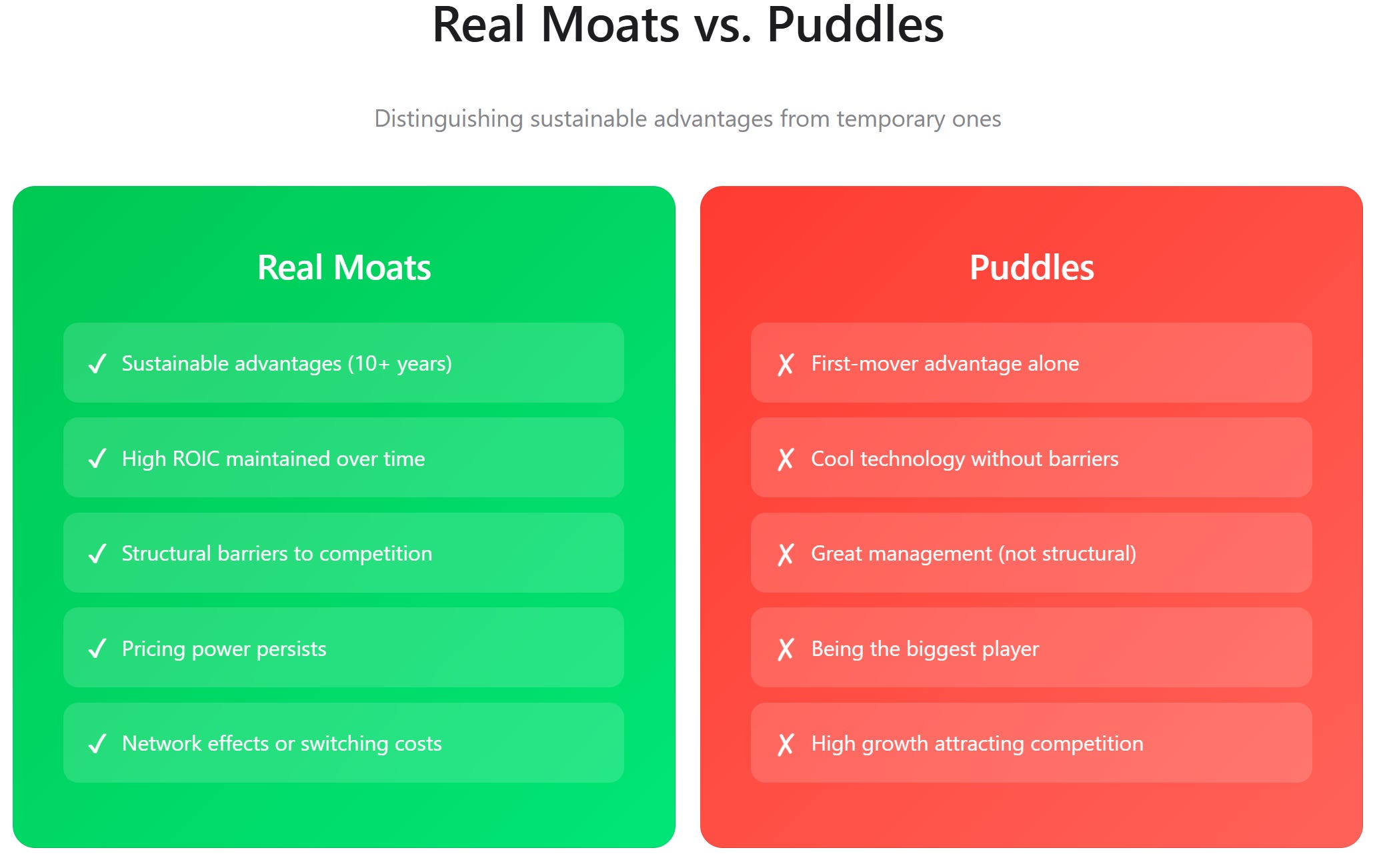

This is where critical thinking separates good investors from great ones. Most alleged moats aren’t moats. They’re puddles.

Puddles dry up.

First-mover advantage is the most overrated fake moat out there. Being first can help you establish scale, brand awareness, and customer relationships. But it’s not a moat because it doesn’t stop others from doing what you do better. MySpace was first in social networks. Friendster came before MySpace. Both disappeared when better competitors showed up.

Being the biggest player gets mistaken for having a moat all the time. Size matters, but size alone doesn’t create lasting advantage. You need the underlying structural reason that size creates advantage.

Great management is wonderful, but it’s not a moat. Management changes. CEOs retire. Key executives leave. A business that depends on one person or one generation of leaders doesn’t have a moat.

Cool technology is incredibly easy to copy. If your advantage is that you have great engineers, so do fifty other companies. Software businesses built on pure technology advantage fail constantly because there’s no moat.

High growth attracts competition like blood attracts sharks. If you’re growing fast, well-funded competitors will flood into your industry. Growth isn’t a moat. It’s the opposite.

The real distinction: competitive advantages are common. Moats are rare. A competitive advantage is anything that gives you a temporary edge. A moat is a sustainable advantage lasting decades.

Most investors buy companies based on temporary advantages and assume they’ll compound forever.

They won’t.

When Moats Fail

Let’s look at three famous cases where investors thought they owned moats but actually owned puddles.

Kodak invented digital photography. The company owned more than seventy percent of the film market and had an unquestionable brand moat. But digital photography destroyed the entire film business. Kodak’s advantages in film manufacturing and brand became worthless when the market shifted.

The lesson: even powerful moats evaporate when the underlying business becomes obsolete. Kodak thought the moat was in film. Actually it was in imaging, and film was just the temporary container. By the time they realized it, they’d lost to Sony and Canon.

BlackBerry dominated smartphone security and had powerful switching costs. Enterprise customers had built entire communication strategies around BlackBerry devices. The switching costs seemed unbreakable. Then the iPhone arrived with a superior experience and Apple’s ecosystem lock-in, and the switching cost moat collapsed.

Customers suddenly found the better experience worth the switching pain.

Blockbuster had convenient locations and a brand that meant “movie rental.” Seemed like a moat. Netflix offered delivery and later streaming, providing so much more convenience that physical locations became worthless. All the local store advantages disappeared overnight.

Your moat is only as good as the technology and consumer preferences surrounding it.

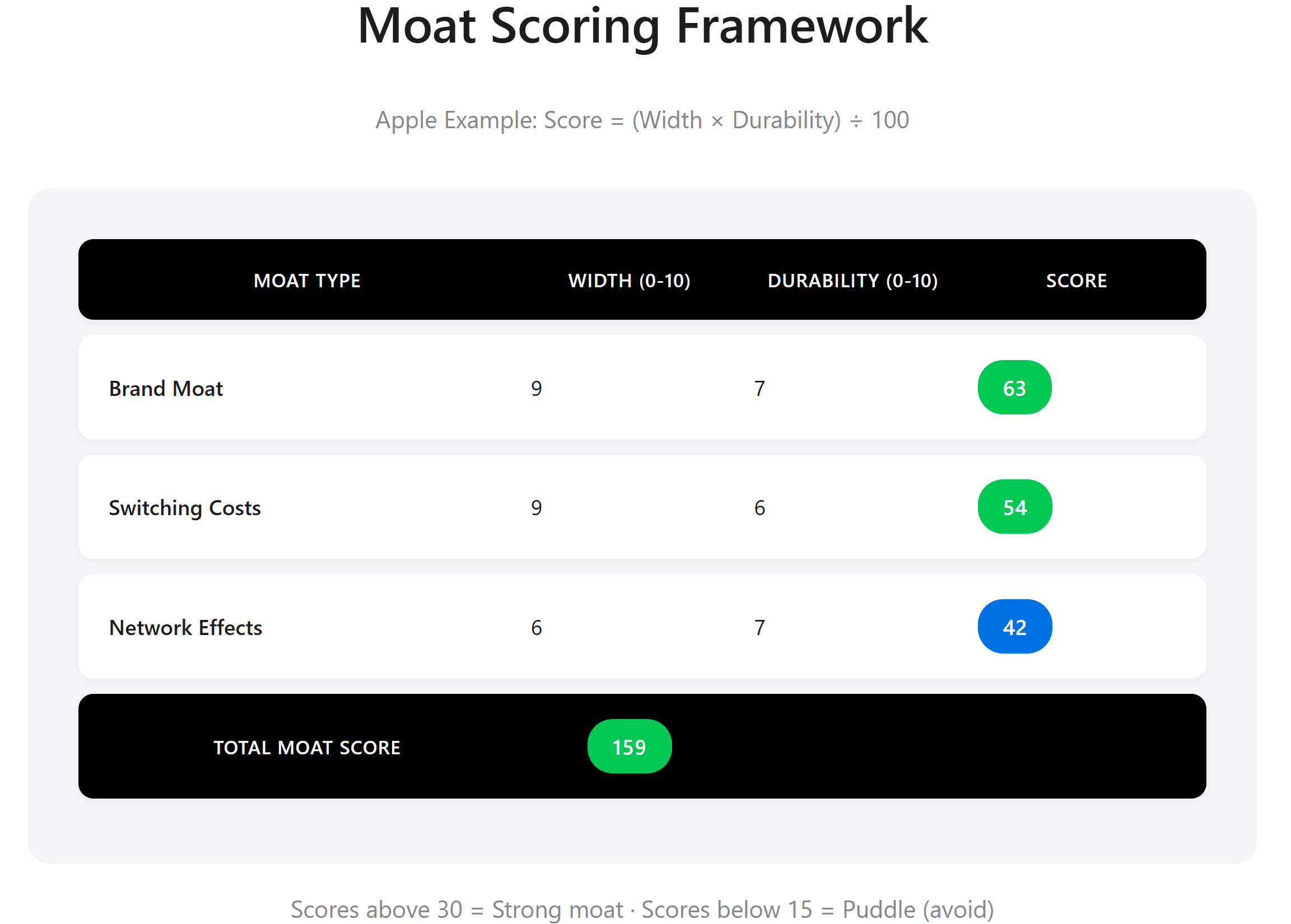

A Practical Framework

Here’s something you can use right now to evaluate any company’s moat.

Rate each of the five moat types on two dimensions: width (how strong today on a scale of 0-10) and durability (how long it will last, 0-10). Then use this formula for each moat type: Moat Score = (Width times Durability) divided by 100.

Let’s work through an example with Apple’s brand moat. Width is probably 9 out of 10 (incredibly strong brand). Durability might be 7 out of 10 (strong but vulnerable to shifting preferences over decades). Score equals 63.

Apple’s switching cost moat? Width is 9 out of 10. Durability is 6 out of 10 (ecosystems can be disrupted by superior competitors). Score equals 54.

Network effects might score 6 out of 10 for width (not as powerful as the other moats) and 7 out of 10 for durability, equaling 42. Here’s what that would look like below:

Add all five moat type scores together. Scores above 30 suggest a strong moat portfolio. Scores below 15 suggest a puddle you should avoid.

This framework isn’t perfectly scientific, but it forces you to think systematically about moat quality and durability instead of just trusting your gut.

What Should You Pay?

This brings us to valuation: how much should you pay for a moat?

The answer depends on moat width and durability. A company with no moat might trade at 8 to 12 times earnings because investors expect competition will eventually crush profits. A narrow moat company might justify 15 to 20 times earnings because the advantage is real but limited. A wide moat company might deserve 20 to 30 times earnings or higher because the advantage will compound for decades.

Buffett’s phrase captures this perfectly: “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

Here’s why. Imagine a wide-moat company trading at 25 times earnings that compounds at 12 percent annually. Over ten years, $100 of earnings grows to $310. The company worth $2,500 (25 times 100) becomes a business earning $310 annually. That’s worth $7,750 if it still trades at 25 times earnings.

Compare this to a company with no moat trading at 10 times earnings. It earns $100 initially but faces intense competition that limits growth to 5 percent annually. Over ten years, earnings grow to $163. The company worth $1,000 (10 times 100) becomes worth $1,630.

You made a much smaller return despite buying at a cheaper multiple.

The math shows why quality matters more than price. Most of the time.

Finding Moats by Industry

Different industries have different structural moat patterns.

Software and tech platforms almost always feature network effects and switching costs. Think about the platforms where moving to a competitor would be hugely disruptive. These are good places to hunt moats.

Consumer brands rely heavily on intangible assets. Where are people paying premium prices because of the brand? These moats can last forever.

Industrial companies often have cost advantage moats built through scale and operations. Look for companies where size creates structural advantage.

Healthcare and pharmaceutical companies build moats through patents and regulatory licenses. Remember though: these moats have expiration dates.

Utilities feature natural monopoly moats. Incredibly stable but often regulated.

Restaurants, retail apparel, and commodity businesses are red flags. Moats rarely exist there. Competition is brutal, switching costs are zero, and scale often doesn’t help.

Modern Threats

Technology is disrupting moats that seemed permanent.

Platform moats are being questioned now. We used to think if you built a platform with network effects, you owned the category forever. But DoorDash beat Seamless. Instagram beat MySpace. TikTok beat Facebook as the social platform for young people.

Network effects are real, but they’re not quite as permanent as we thought.

AI could fundamentally disrupt switching cost moats. If AI can help companies migrate off legacy software platforms more easily, switching costs decline. If AI makes software infinitely customizable, brand advantages might erode.

Direct-to-consumer brands are trying to bypass distribution moats by selling straight to customers. Sometimes they win, sometimes they don’t.

No moat is truly permanent. Every moat requires constant monitoring and questioning.

How Buffett Actually Uses This

Looking at how Buffett actually applies moat analysis to his portfolio teaches practical lessons.

His biggest holdings reflect clear moat preferences. Apple combines brand, switching costs, and network effects. Coca-Cola is pure brand moat. American Express is switching costs and network effects. Bank of America has cost advantages and switching costs.

Notice what’s missing from Berkshire’s largest holdings: businesses in competitive industries with no moats, purely growth-based stories without sustainable advantage, and businesses where moats are visibly eroding.

Buffett doesn’t evaluate moats in isolation. He also evaluates management quality, capital allocation discipline, and valuation. Even a wide-moat company is a bad investment if management is incompetent, capital is being wasted, or the price is ridiculous.

The moat is necessary but not sufficient.

Your Time Horizon Matters

How much moat quality matters depends on your time horizon.

For a three to five year hold, even a narrow moat might work. You’re betting the company stays dominant during your holding period. But you need an exit plan because the moat will eventually narrow or vanish.

For a ten-year hold, you need a wide moat. The advantage needs to be durable through at least one business cycle and technological evolution.

If you’re thinking like Buffett, planning to hold forever, you need moats that can last through multiple business cycles, regulatory changes, and technological revolutions.

Very few companies qualify.

Test durability by imagining the business in 2050. Can you still see a moat? If not, it’s not durable enough for forever.

Building Your Portfolio

Should you only own wide-moat stocks? In theory, absolutely. In practice, it’s harder.

A reasonable allocation: 60 percent wide-moat stocks forming your core, 30 percent narrow-moat stocks purchased only when prices are attractive, 10 percent special situations and higher-risk bets.

This keeps you focused on quality while allowing flexibility. You also get diversification across different moat types, which reduces correlation between holdings. A regulatory threat that destroys switching cost moats won’t affect brand moats.

Monitoring Moat Health

Create a system for checking whether your moats are still moats or becoming puddles.

Quarterly, read earnings calls and financial reports looking for warning signs. Annually, score your major holdings using the framework from earlier. Ask yourself honestly:

Have competitors gained share? Has pricing power changed? Are customer retention metrics stable? Is the industry’s competitive dynamic shifting? Are new regulations emerging? Is technology threatening the moat?

When you spot clear evidence of moat erosion, not just temporary headwinds, consider selling.

Your Moat Checklist

Use this checklist to evaluate any company:

What prevents competitors from copying this business? Why can’t a well-funded startup replicate this? Will this advantage matter in ten years? What would destroy this moat? Which of the five moat types apply? Is this a real moat or just a puddle? How wide is the moat (ROIC versus cost of capital)? How durable is the moat (can it survive ten years)? What’s the first sign that this moat is eroding? Is the current valuation reasonable given moat quality?

Answer these questions honestly, and you’ll make better decisions than most investors.

The greatest investment breakthroughs happen when you stop mistaking temporary advantages for permanent ones. That’s what Buffett learned with See’s Candies in 1972, and it’s as relevant today as it was then.

Find real moats. Stack multiple moats when possible. Pay fair prices for wide moats. Monitor constantly. Distinguish between castles and puddles.

Your returns will follow.